Energy Shock, Rate Surge Push World Economy Into ‘Spikeflation’

Forecast Trend Report by Period

Prices Jump Suddenly After Middle East War

‘Time to Rebalance Investment Portfolios’

The world economy is entering a phase of “spikeflation,” with prices rising in sudden bursts rather than gradually, amid mounting cost pressures led by energy after the recent Middle East war.

The Financial Times reported on June 4 that signs of spikeflation have appeared in the global economy since the war in the Middle East began in late February. Geopolitical tensions, energy and supply-chain risks, and shocks from government fiscal policy are combining to drive abrupt price increases.

Global oil prices have climbed to their highest level in four years. The International Energy Agency has described the current energy crisis as delivering “twice the shock” of the 1970s oil crisis. The impact is feeding through to inflation worldwide. In the US, the personal consumption expenditures price index rose 3.8% in April from a year earlier, the largest increase since May 2023.

That backdrop is poised to weigh directly on asset markets. The FT’s analysis of asset-price moves since 1915 found that stocks and bonds both delivered weak returns during spikeflation periods. Government bond yields have already jumped sharply, sending prices lower. The 30-year US Treasury yield reached 5.2% in May, its highest level since 2007.

Trevor Greetham, head of multi-asset at Royal London Asset Management, said other asset classes, including equities, showed a similar pattern during spikeflation periods. Although the S&P 500 has recently climbed to a record, the risks from persistently high inflation remain. Investors need to diversify portfolios through commodities and other inflation hedges, he said.

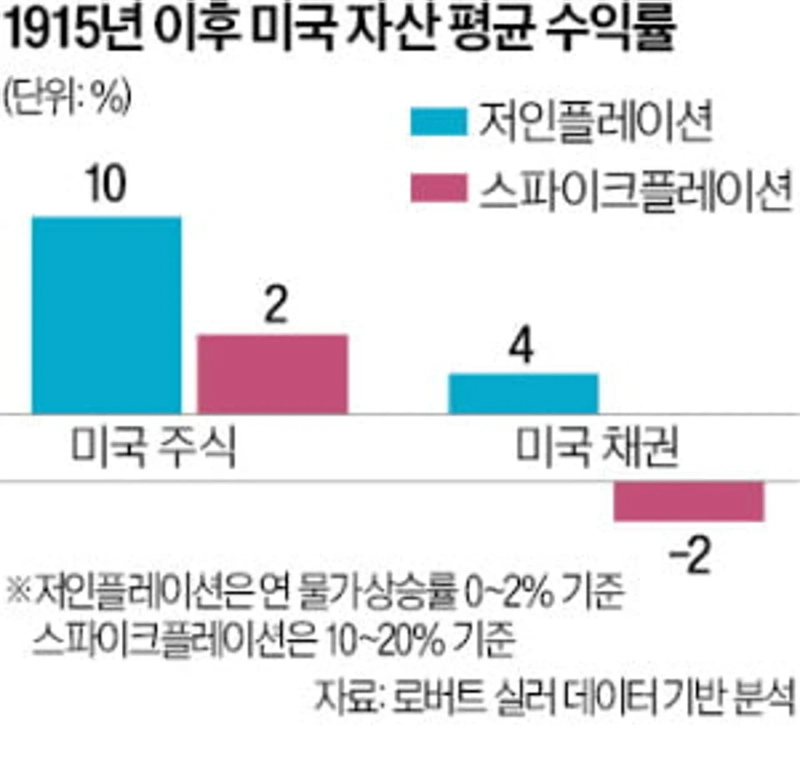

US Stocks Return 10% a Year During Stable Inflation Periods

But That Shrinks to 2% During Inflation Spikes

Spikeflation refers to a sudden acceleration in inflation after a prolonged period of subdued price growth, driven by a combination of geopolitical shocks, energy bottlenecks, fiscal excess and supply-chain disruption. A lengthy stretch of low inflation is effectively a precondition for spikeflation, making its impact on the economy and asset markets especially severe.

G20 Inflation Forecast to Rise 4.0%

The Organization for Economic Cooperation and Development said on June 4 that the recent Middle East conflict is projected to lift consumer inflation across the Group of 20 economies to 4.0% this year from 3.4% last year.

If disruptions to Middle East energy production and exports persist through the second half of next year, inflation could rise by an additional 0.4 percentage point this year and 1.3 percentage points next year, the OECD said. Under that scenario, global growth would slow to 2.1% this year and 1.8% next year.

Governments have limited room to respond. In its April Fiscal Monitor, the International Monetary Fund said global public debt rose to 94% of gross domestic product last year and projected that it would reach 100% by 2029. The increase reflects a simultaneous surge in spending on social programs, defense, strategic industries and interest payments on government debt.

The IMF has also said the recent Middle East conflict will further deepen fiscal vulnerabilities across governments. That is why absorbing the inflation shock through public spending is becoming more difficult.

The shift is also affecting investment assets. Royal London Asset Management found that US stocks returned more than 10% a year on average during periods when inflation remained below 2%, while US Treasuries returned 4% annually. During spikeflation periods, however, stock returns fell to below 2% a year and Treasuries posted annual losses of 2%.

Unusual Stock Rally Also Carries Risks

Markets are already starting to reflect the effects of spikeflation. The 10-year US Treasury yield has recently risen to 4.45%, while the 30-year yield has climbed to around 5%. Last month, the auction yield on 30-year Treasuries moved above 5% for the first time since 2007, underscoring the drop in returns for bond investors.

In April, US homeowners withdrew 5.8% of all homes listed for sale. Expectations had grown that the Federal Reserve would raise its benchmark interest rate to the highest level since the Covid-19 pandemic. Higher borrowing costs lead buyers to demand lower prices, and sellers who refuse often pull listings from the market.

Still, the S&P 500, the main US stock benchmark, has returned 14% this year on enthusiasm for artificial intelligence-related investment. Vanguard’s S&P 500 ETF, VOO, also recently became the first exchange-traded fund to surpass $1 trillion in assets under management. Because the ETF is weighted by market capitalization, rallies in AI-related and other large technology stocks automatically increase their share of the portfolio.

A Royal London Asset Management official said investors risk losses if they fail to respond properly when persistent inflation shocks hit markets. Investors should cut risk by adding commodities and other inflation hedges to their portfolios, the person said.

Kim Ju-wan, Hankyung.com reporter kjwan@hankyung.com

Korea Economic Daily

hankyung@bloomingbit.ioThe Korea Economic Daily Global is a digital media where latest news on Korean companies, industries, and financial markets.